Stakeholder Liaisons

Doug Blade

Karen Brehmer

Neki Cox

Kathleen Fox

Stakeholder Liaison Manager

Kristen Hoiby, Area 6 manager

Departments of Revenue

MO Laura Wallendorf

NE Dawn Holtmeier

Tax Professionals

Rita Barnard

Darrel Beadle

Velma Bjorgum

Jacob Borash

Frank Carnahan

Brad J Decker

Kelly Golish

Jacen Gondringer

Doug Gross

Steven Heeley

Cindy Hockenberry

Terry Johnson

Bill Kelly

Rick Kollauf

Ken Larsen

Judy Lashinski

Terri Lillesand

Laura Merschman

Ruth Ann Michnay

Holly Muehl-Pett

Paul Osterberg

Jodee Paape

Kathy Reiniger

JoAnn Schoen

Barbara A Steponkus

Brad Voght

Jill Wrensch

No webinars scheduled at this time. Please check Webinars for Tax Practitioners for upcoming webinars.

Discussion items

1) 2019 Form 1040 and schedules

2019 Form 1040. There are three schedules for 2019, compared to six in 2018.

- 2018 Schedule 6 Foreign Address and Third Party Designee is now incorporated into the 2019 Form 1040 and no longer exists

- 2018 Schedule 5 and 2018 Schedule 3 are combined into Schedule 3 for 2019 Additional Credits and Payments

- 2018 Schedule 4 and 2018 Schedule 2 are incorporated into Schedule 2 for 2019 Additional Taxes

- Schedule 1 Additional Income and Adjustments to Income is still in use.

- New for 2019 is this virtual currency question added above line 1 for this schedule: At any time during 2019, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?

2) Virtual Currency

- Landing page at IRS.GOV for Virtual Currencies

- FAQs and resources

- IRS Criminal Investigation releases Fiscal Year 2019 Annual Report; celebrates 100 years. Key focus of CI in fiscal year 2019 included cybercrimes, with an emphasis on virtual and crypto currencies, traditional tax investigations, international tax enforcement, employment tax, refund fraud and tax-related identity theft. Other areas of emphasis included public corruption, corporate fraud and money laundering.

3) Discussion: Form W-4 for 2020, federal and state rules

NEBRASKA:

For 2020, if an employee changes withholding, they must use the new IRS Form W-4. In Nebraska, the employee MUST ALSO fill out a new W-4 for the state of NE.

MINNESOTA:

Mark Krause provided this information: Beginning January 1, 2020 when a new employee fills out a W-4 or an existing employee changes their W-4, a new 2020 W-4MN will need to be completed since withholding allowances will no longer be calculated on the federal W-4. The rules for submitting a W-4MN to Revenue have not changed.

WISCONSIN: Changes to Form WT-4

- The Internal Revenue Service has redesigned Form W-4 for the year 2020. As explained in the DRAFT posted on the IRS website, federal allowances have been removed. Prior to this change, an employee could use Form W-4 for Wisconsin purposes if the employee’s federal allowances equaled his or her Wisconsin exemptions. Since federal allowances have been removed, the redesigned Form W-4 cannot be used for Wisconsin purposes.

- The following applies for Wisconsin withholding tax purposes beginning in 2020:

- All newly-hired employees must provide Form WT-4 to their employer.

- Existing employees that change the number of their Wisconsin withholding exemptions must provide Form WT-4 to their employer.

- Existing employees are not required to provide Form WT-4 to their employer (unless the employer requests it) if the employee wishes to maintain the same number of Wisconsin withholding exemptions used in 2019.

MISSOURI:

Laura Wallendorf will look into this issue.

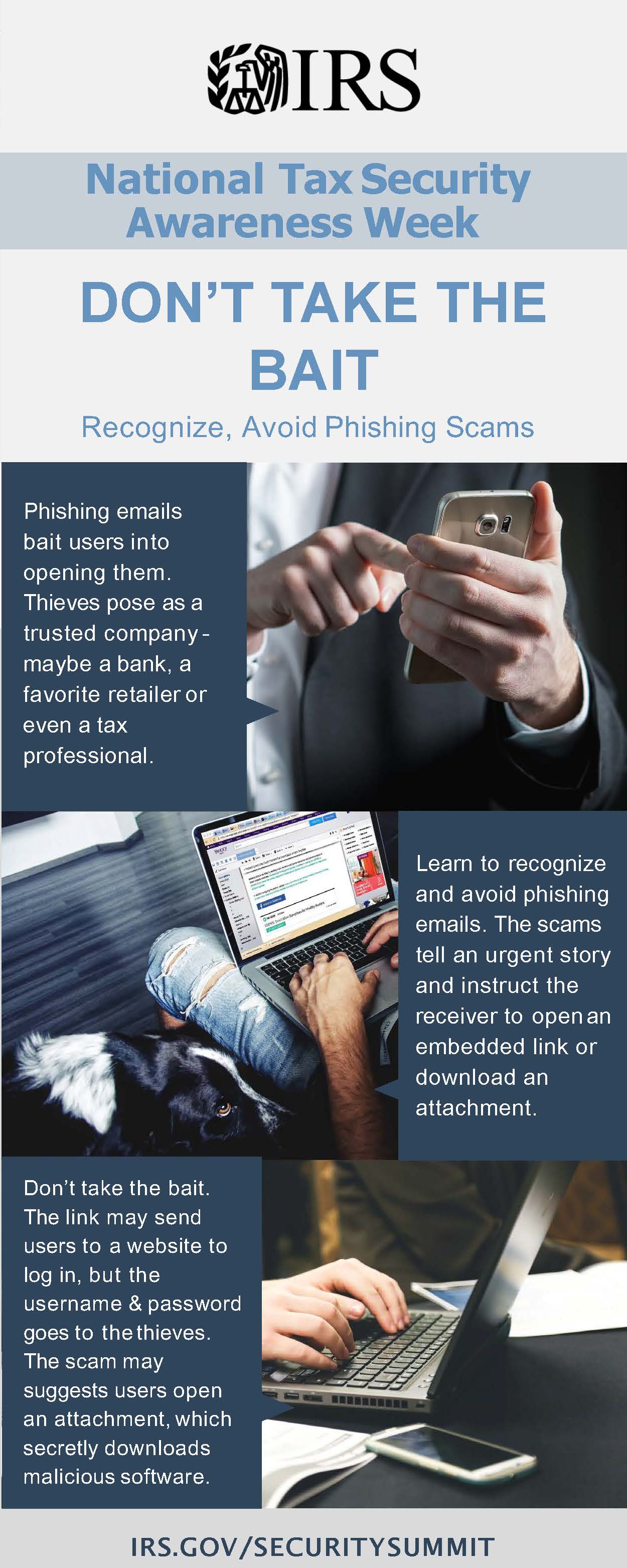

4) National Tax Security Awareness Week

- IR-2019-192, National Tax Security Awareness Week begins; IRS and Security Summit partner offer Cyber Monday shopping tips to protect computers, mobile phones

- IR-2019-195, National Tax Security Awareness Week, Day 2: Don’t take the bait: Recognize, avoid phishing scams from identity thieves

- IR-2019-196, National Tax Security Awareness Week, Day 3: Creating strong passwords can protect taxpayers from identity theft

- IR-2019-198, National Tax Security Awareness Week, Day 4: IRS, Security Summit warns business owners about being targets for identity thieves

- IR-2019-200, National Tax Security Awareness Week, Day 5: Tax professionals need data protection plans; must guard against identity theft

5) IRS reminds tax professionals of tasks to get ready for 2020

- Update e-Services information

- Renew PTINs

- Update POA/third-party authorization records

- Review security safeguards

- Review Practitioner Priority Service options

- Register for e-News for Tax Professionals and subscribe for quick alerts

State Departments of Revenue

Minnesota – Mark Krause

- Each day we are mailing approximately 3,000 tax year 2017 conformity-related adjustment letters. Our goal is to be completed with 2017 adjustments by the end of this year.

- Any questions can be directed to [email protected].

Your issues and questions:

1) Taxpayer First Act

There are three issues that commonly come up and have been an issue for many years. Please use the Taxpayer First Act email to share these concerns with the IRS.

1) Letters or payments “cross in the mail”. Example: The taxpayer pays a balance due on Form 1040 by check or by Electronic Funds Withdrawal on 10-15-2019. The taxpayer gets a balance due notice in early November. The IRS system does not show the payment.

2) The taxpayer gets a paper refund check as a result of an adjustment after their return has been processed. They already received the original refund as shown on the return, or they paid the balance due. Or they get a refund check that is different from what they were expecting. The taxpayer is supposed to get a letter to explain the refund. Sometimes they get a letter up to three weeks after the refund check, or they don’t get a letter at all.

3) Form 2848’s are not processed by the CAF unit in one week, as the IRS states. It often takes three weeks. Sometimes they are not processed at all, and often there is no correspondence to the taxpayer to explain if there was a problem. POAs can’t wait three weeks to contact the IRS, so they call PPS and fax in Form 2848. This works, but it would be better to have an electronic system for submitting Form 2848 where it’s recorded in day or two.

Next Call

The next call will be on January 2, 2020.

We’ll send out the WebEx link closer to that date

Meetings are one hour long. Come when you can, leave when you must.

Thank you to everyone who attended. We appreciate your time and input!